SBC102 case

CASE STUDY:

FINFUL – SOCIAL BUSINESS OPPORTUNITY CREATION

AND BUSINESS MODEL CANVAS

Product and Market

Major Markets:

Target market in general: Gen Z (age range: 15-25, age group 10-18, 18-22, 22-25)

When should people learn about financial literacy?

According to CNBC (2020), the best age to teach financial literacy is from 13-21 (teen and young adults) to help them prepare for important decisions about finance at the age of 18. Other research showed different results, such as those from 16 or higher education, etc.

But the majority of research suggests that parents should start approaching their children about money as early as possible (Pre-K or the first years of primary school)

→ It is never too early to teach children about money.

Why Gen Z?

-

Gen Z concerns about their finance with high demand in spending, tendency to be independent and other personal desire (VietnamBriefing, 2019)

-

Gen Z has the highest internet penetration rate among other groups (90% for gen Z and 78% for millenials) and they are very reliant on mobile phones

Why Finful?

-

There are different factors between urban, suburban, and rural that impact significantly on financial literacy such as income, education, demands, new technology service,etc.

-

However, according to Cimigo, the urban versus rural digital disparity in Vietnam is minimal, the research showed that whilst urban Vietnamese use 4.6 platforms on average, rural Vietnamese use 4.5 on average.

→ A free app gives young people equal opportunities in learning about financial literacy regardless of regions, income, culture, education, etc. by taking advantage of the high penetration internet rate across Vietnam.

Demand

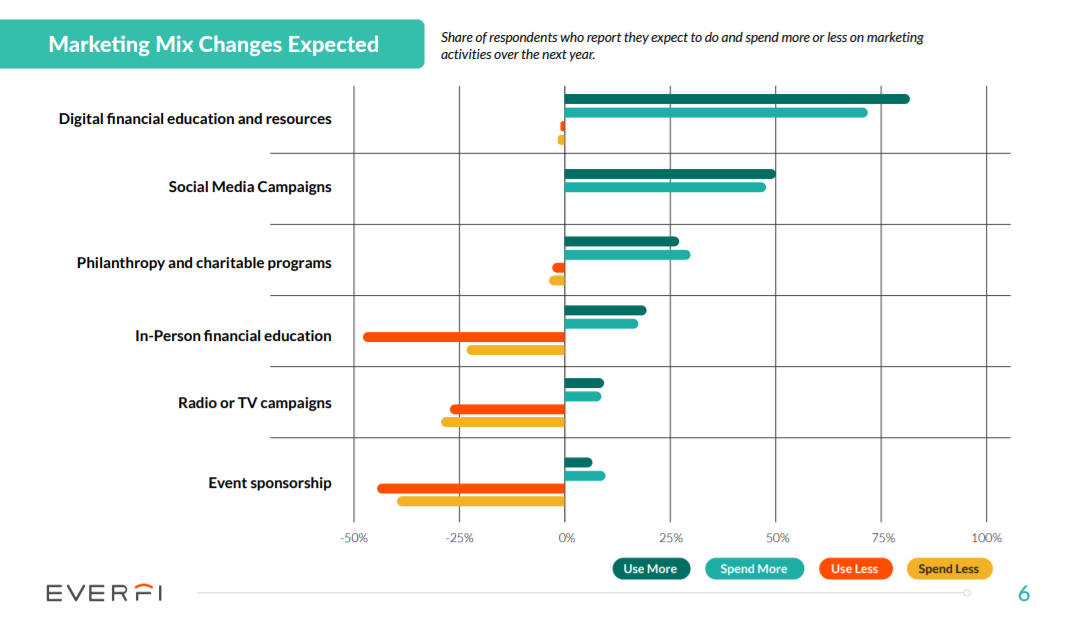

Consumers Seek Financial Education during the Covid-19’s uncertainty

-

The number of unique visitors who reached financial information sites is double. When it comes to brokerages and investment corporations, it was pointed out that users come to sites on a more frequent basis and for a longer period of time (Ferguson, 2021).

-

89% of respondents agree that lack of financial education contributes to some of the biggest social issues our country faces, including poverty (58%), lack of job opportunities (53%), unemployment (53%) and wealth inequality (52%)

Banks and financial literacy demand for customers:

-

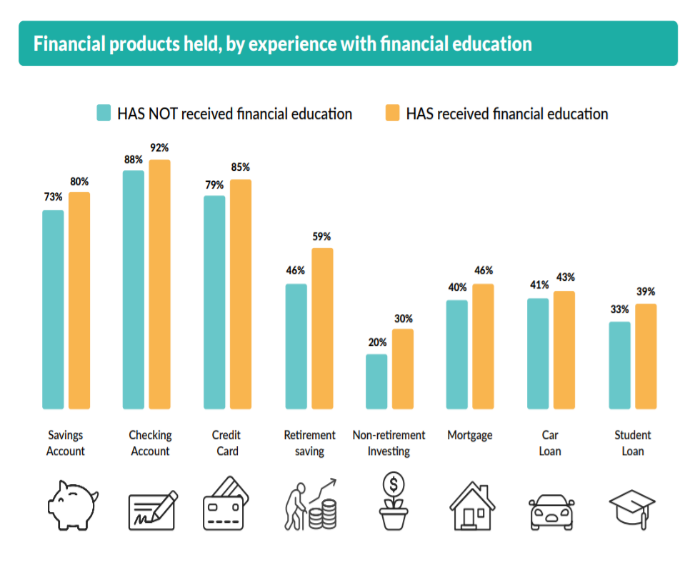

83% of respondents agreed that financially knowledgeable university consumers are important to the future success of their institutions.

(Sources: Everfi, 2020)

-

The data showed that when it comes to comfort engaging with financial institutions, across all income levels there is more willingness to engage among consumers who had financial education in the past

-

Most consumers say financial education would help them engage with their financial institution, but just one in ten have received financial education from a bank or credit union.

Competitive Landscape

Market Share

EdTech industry is categorized by their main focus. But please note that the categories in the market map are not mutually exclusive. As such, Finful will belong to the Broad Online Earning (Life Long Learning) group and will be focusing on personal finance knowledge. This sector in Vietnam so far is fragmented with little to none direct competitors both in urban and suburban areas.

-

Therefore, this is an opportunity for Finful to consolidate and capture the market

Majority of EdTech startups follow the Direct-to-Consumer while at this stage, Finful will primarily focus on providing free lessons for consumers and revenue stream will be from B2B model.

-

More accessible and easier to acquire customers since it is free

Success Factors

What differentiates Finful from potential competitors is that Finful creates an easy-to-use, comprehensive and free financial literacy solution for Gen Z with different levels/ backgrounds. We combine gamification and learn-to-earn (partnering with banks under the B2B model). From here, Finful generates income and simultaneously increases user retention, learning effectiveness.

By offering a learning solution, Finful solves banks’ problems and financial literacy demands of Gen Z:

-

We can take full advantage of technology trends (edtech, fintech, gamification) and current trends (investment demands among Gen Z, banks’ issues).

-

Through that, our app can improve users’ financial literacy and facilitate the economy of Vietnam as a whole.

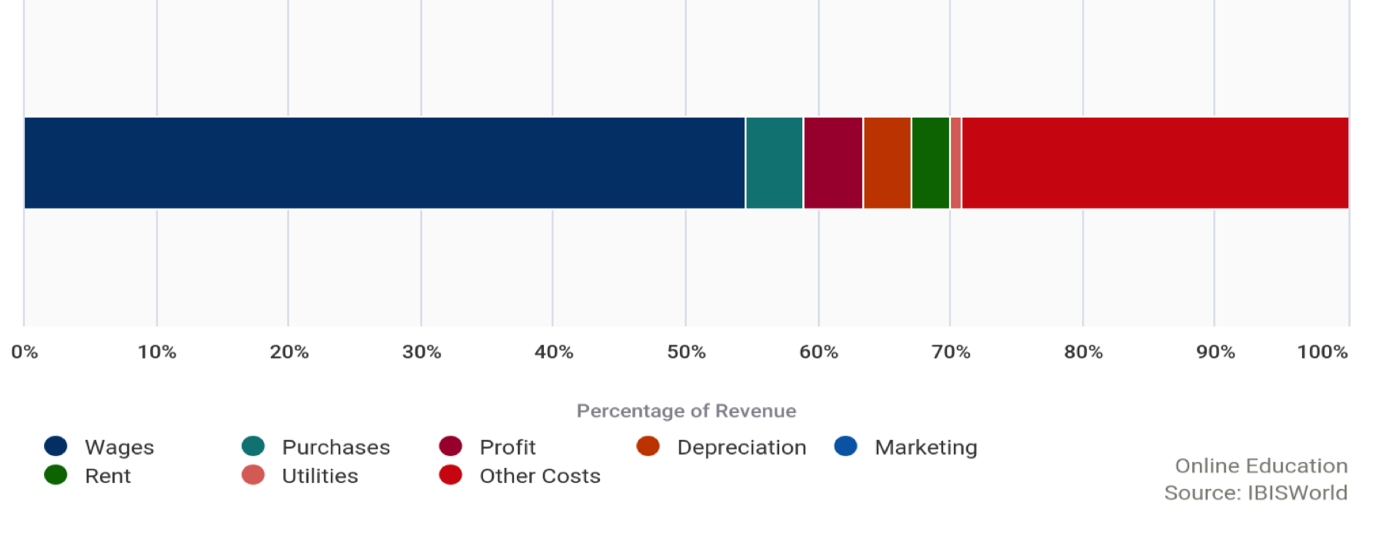

Cost Structure

Please note that the cost structure above should be taken with a grain of salt as this industry is fairly new to the Vietnam market, with different business models comes with different cost structures. But we’ve identified that the majority of expenses are for wages, and marketing costs.

Wages

Providing education and building applications typically incurs high labor costs, as developers, content writers, industry professionals are essential for the building of application and contents. High quality content as well as high-end technology outcomes are necessary for Finful to remain competitive

Marketing

The industry’s marketing expenditure is significantly high as the result of expanding the number of customer bases, reaching out to potential business partners, etc. Marketing expenses are usually associated with the cost of listing on the website, and partnership with other organizations. Finful needs to constantly invest in marketing initiatives to increase their presence and compete with established online education providers. However, Finful can take advantage of many free platforms to decrease the total of marketing costs.

Competition

What sets us apart from all of our competitors is our learn-to-earn model, which enables users to earn money while learning. We also managed to improve our interaction within the app by applying gamification model

Barrier to entry

We break down the barriers model by deeper analysis as following:

Table 1. Barriers to entry’s factors analysis

Source: Finful team’s compilations

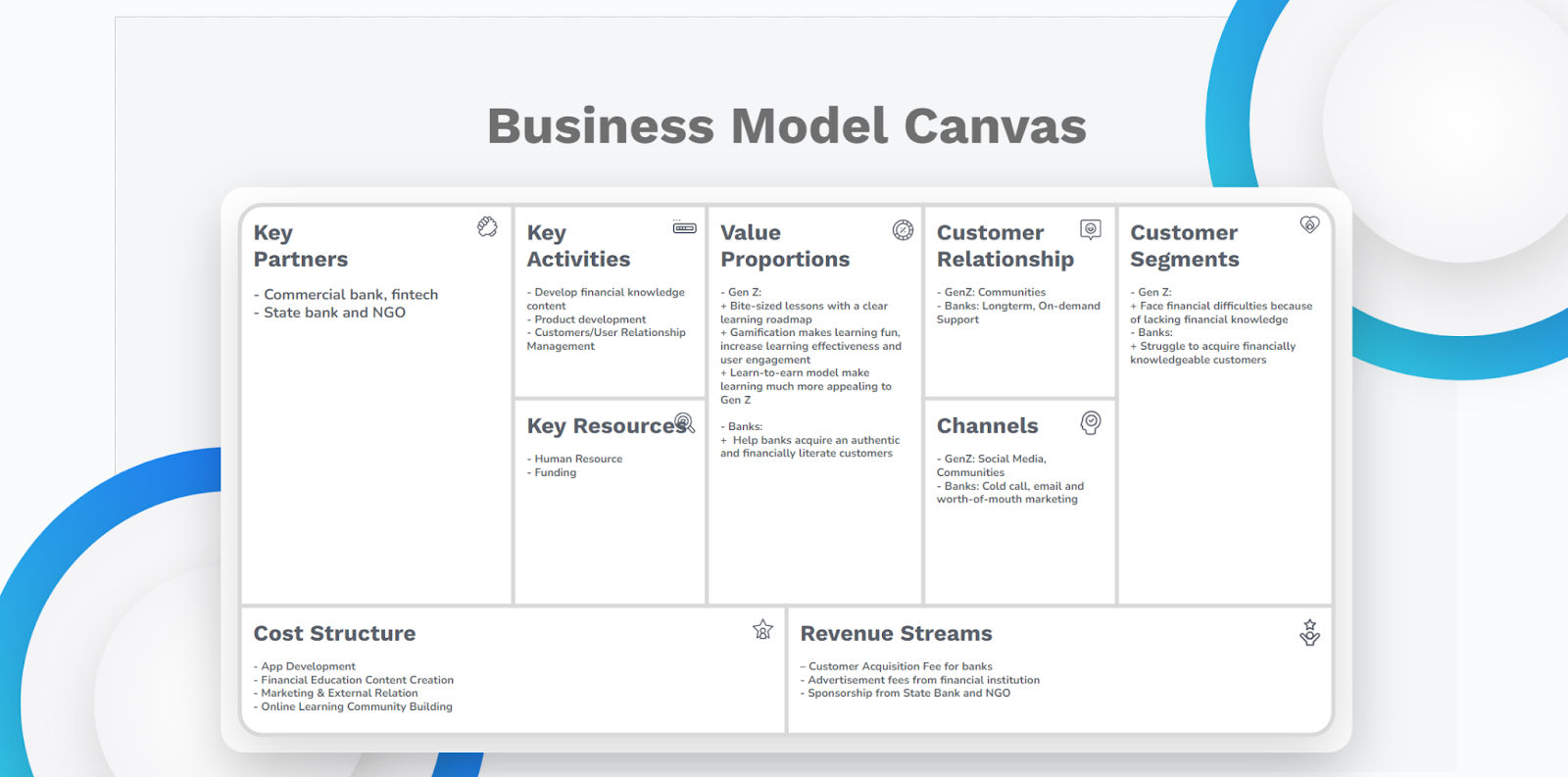

Business Model Canvas